By Hardik Pandit, Director of APICES Studio Pvt. Ltd.

India is undergoing an economic transformation. From nimble startups to growing conglomerates, businesses are expanding like never before. However, as the ambitions for growth increase and the number of employees expands, a major question arises: what will be the operational base of these companies? The availability of high-quality, well-placed offices is not keeping pace with the relentless demand. The shortage of office spaces is turning into a big hurdle, especially in cities like Bengaluru, Mumbai, Pune, and Hyderabad.

Increased demand, reduced supply

The issue of commercial-grade A office spaces is particularly acute in India. As per the latest reports from various consultancy organizations, the resurgence of IT, fintech, and global capability centers (GCCs) has been facilitating the demand for Grade A office space during the period of 2023-2024. However, meeting the demand is constrained because of postponed construction timelines, scarcity of land in prime regions, and post-pandemic regulatory red tape.

The pressure is particularly acute in Tier 1 cities. For instance, the average vacancy rate in prime micro-markets in Bengaluru is now below ten percent. This is not only alarming for investors but also occupiers. Other dynamic areas like BKC and Lower Parel in Mumbai are similarly strained, where rental prices continue to climb and new inventory is not being supplied by builders.

The surge of startups and the GCC boom

Funding and recruiting in India is booming, and this is largely driven due to the numerous start-up opportunities available. Alongside this, there is a surge in international companies setting up or expanding their Global Capability Centers (GCCs) in India. These centers have evolved beyond their traditional roles as mere support centers; they now serve as critical innovation hubs. This leads to the increased demand for collaborative workspaces that are tech-enabled.

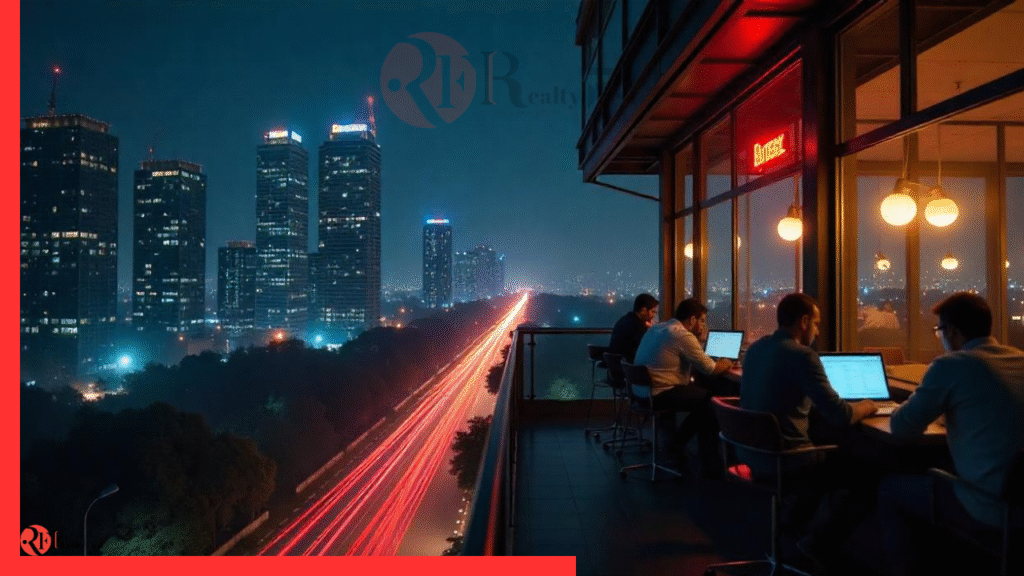

The transformation of workplaces has been further accelerated by the pandemic. Companies have started to prefer offices with open layouts, breakout areas, video conferencing facilities, wellness rooms, and energy-efficient systems. Employees are now more willing to work overtime when these systems are in place, so they improve engagement and productivity.

The flexible and co-working models are increasingly popular, but even these providers are running out of available space. There’s now a shrinking amount of space available for large enterprises looking for full-floor customisation or long-term leases. In addition, companies are becoming highly selective in terms of location and amenities, making leasing even more complicated.

Infrastructural and regulatory bottlenecks

One of the other key issues is the speed at which permissions and clearances are granted. Developers cite lengthy processes for environmental clearance, change-of-land-use permissions, and other statutory hurdles as causes for delay. These regulatory inefficiencies slow down the construction of commercial buildings and limit foreign investments.

In addition to this, several infrastructure projects that are, or already are, expected to bring new business opportunities are themselves delayed. In cities like Pune and Hyderabad, lack of coherent urban planning has worsened traffic congestion and new business growth.

The difficulty of the situation is worsened by the lack of readily available green materials and expertise for sustainable, green-certified buildings. ESG efforts appreciate the attempt, but these projects take longer and are much more expensive. The adoption of LEED or IGBC certifications also requires sophisticated HVAC systems, advanced water recycling, and smart lighting, which further add to development time and costs.

Do tier 2 cities provide a solution?

As tier 2 cities such as Indore, Coimbatore, Jaipur, and Ahmedabad gain infrastructure sophistication, they are drawing the attention of many firms, including the likes of TCS, Infosys, and Accenture. These firms establish satellite offices in the region. Startups and SMEs are also looking to set these cities for backend operations and support services owing to the lower operational expenses.

So far, these cities face numerous challenges, including talent relocation, lack of grade A office space, absence of mature business support systems, and poor interstate air travel. Furthermore, with an unreliable power industry and overseas amenities, these cities cannot accommodate foreign buses or employees. Thus, while tier 2 cities look promising, they do not resolve the immediate space issues.

Flexible workspaces: The next step or an intermediate step?

The increase in demand resulted in the need for additional office space, and as a result, managed offices and co-working spaces emerged. Companies such as WeWork, Smartworks, and Awfis expanded aggressively in the last two years, offering enhanced plug-and-play convenience, shorter lease durations, and community-centered designs.

The appeal they offer has surged along with the adoption of hybrid work models. Employees have a greater preference for choice and flexibility. For businesses, co-working spaces offer reduced CAPEX, increased agility, and scalable solutions. This makes them attractive for everything from short-term engagements to client-interfacing teams.

Nonetheless, flexible workspaces still cannot substitute headquarters or client-facing offices for larger companies. While they cater best to early-stage startups or project-based teams working in hybrid structures, the commercial real estate market still needs to build robust core inventory. This is especially true in BFSI, legal, or pharma industries where data security, confidentiality, and compliance are mandatory deal-breakers and tailored, owned spaces are prioritized.

Policy push and developer strategy

Both government action and private development initiatives are necessary to resolve the crisis. Streamlined single-window clearances, digitization of land records, and acceleration of infrastructure projects are all capable of alleviating critical bottlenecks. Long-term relief may also result from incentivizing green buildings, tax deductions for commercial construction outside core zones, and releasing dormant government land.

As for the developers, they are now exploring vertical business parks as well as transforming old industrial estates into business hubs using modular construction methods to accelerate delivery. Some are partnering with city planners to incorporate commercial centers into walkable mixed-use urban developments. There is also a revival in the retrofitting of obsolete office buildings to modern standards, making them desirable alternatives to new constructions.

Commercial real estate infrastructure is also being financed and expanded through real estate investment trusts (REITs). By consolidating investor funds and focusing on sustained long-term returns, REITs bring liquidity and scale to this otherwise stagnant industry.

The workspaces that propel India towards a $5 trillion economy must remain an enabler of growth, not a hindrance. Coordination amongst the government, developers, and occupiers is vital to achieve balanced and dependable advancement in the commercial real estate sector.

Key takeaways:

- India’s economic growth is triggering an unprecedented demand for high-quality office spaces.

- Supply is lagging due to regulatory delays, land scarcity, and construction backlogs.

- Startups and GCCs are key demand drivers, often requiring flexible yet scalable infrastructure.

- Tier 2 cities offer potential but face their own growth hurdles, especially in attracting top talent and building urban ecosystems.

- Co-working spaces provide temporary relief but aren’t a long-term solution for all types of businesses.

- Policy reforms, green incentives, and innovative developer strategies—like modular construction and adaptive reuse—are essential to resolving the office space crunch.